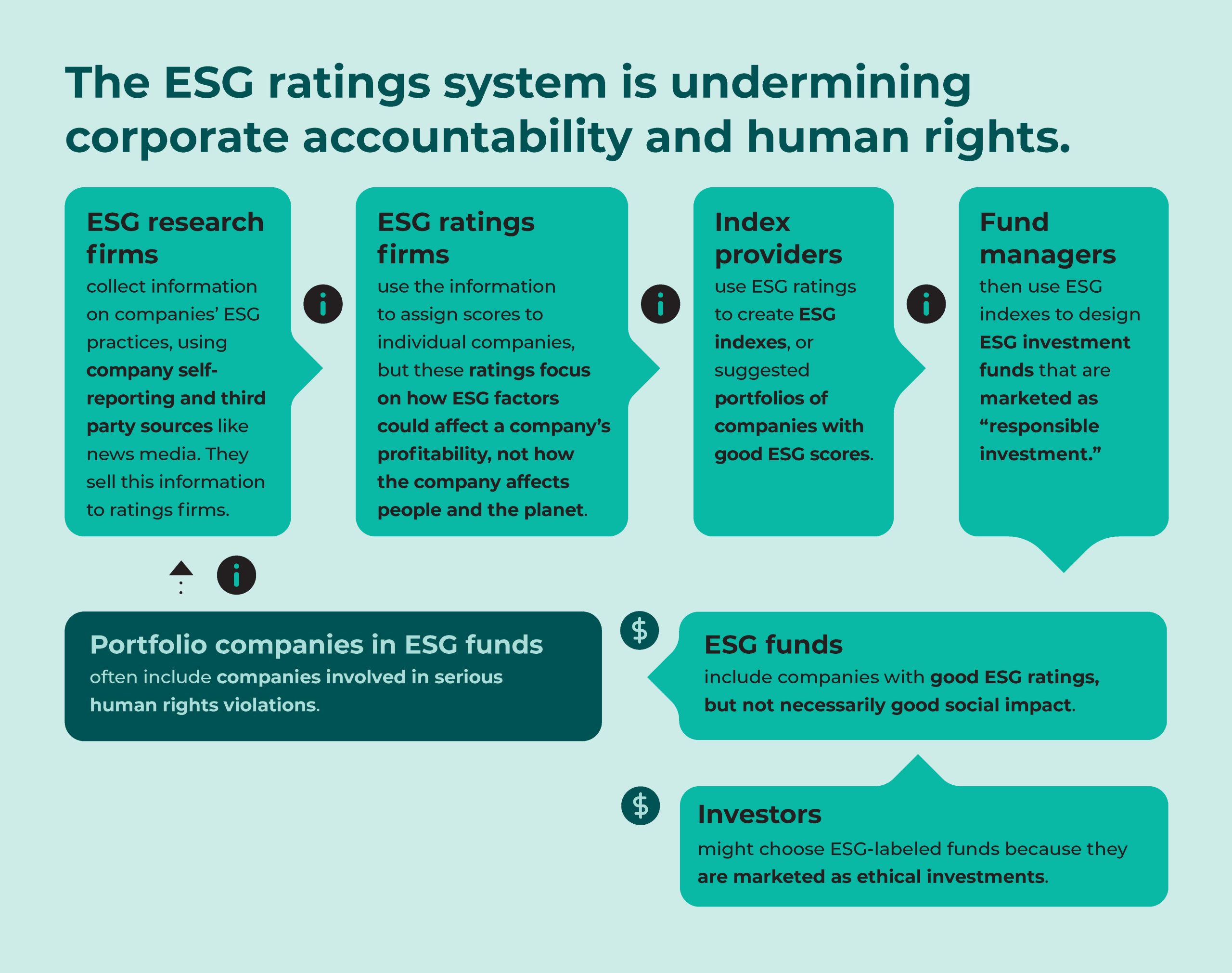

Asset managers advertise ESG investment funds as a way for everyday investors to align their money with their values. But contrary to what the average investor would expect, the ESG ratings used to tailor investment portfolios and determine which companies benefit from ESG investment often disregard evidence of a company’s negative impact on communities, workers and the environment.

Even when such evidence is considered, ESG ratings can mask human rights abuses and other destructive corporate behaviors because they combine a wide range of environmental, social and governance indicators into a single score. That means a company can offset bad behavior in one area—e.g., land grabbing or use of forced labor—with unrelated initiatives in another—e.g., launching a new recycling program or improving the diversity of its board.

ESG index providers are firms that translate ESG ratings into ESG investment indexes, which greenlights those companies for inclusion in ESG-labeled investment funds (i.e., funds with names that include phrases like “ESG Leaders” and “ESG Screened”). The leading index providers—MSCI, FTSE Russell and S&P Dow Jones Indices—have become the gatekeepers of trillions of dollars in capital, giving them enormous leverage with companies seeking a spot on their indexes. They can use that leverage to ensure the companies they are promoting as “responsible investments” are not involved in human rights abuses. In fact, they have a responsibility to exercise that leverage under the UN Guiding Principles on Business and Human Rights, but they almost never do.

The low bar for securing a place in ESG funds helps direct “responsible investment” to the wrong place, and it makes it harder to hold some of worst corporate offenders accountable. We know from first-hand experience in our casework that the “ESG” stamp of approval undermines the efforts of communities and human rights defenders to secure redress for corporate abuses by making investors less likely to engage with a company and use their leverage to compel action.

Inclusive Development International launched the ESG Watch website and company database to put a spotlight on the problem of ESG-washing, and to hold the ESG investing industry accountable. The database tracks tens of billions of dollars in ESG-focused investment flowing to companies that are linked to serious social and environmental harm. ESG Watch provides a platform to amplify the voices of communities affected by harmful corporate activities, publicize evidence of harm and hold financial services firms and investors accountable for fulfilling their human rights responsibilities.

We are working with civil society partners and affected communities around the world to add new companies to the database on an ongoing basis, and to hold them and the ESG investment industry accountable. Visit the website to learn more.

In February 2024, Inclusive Development International filed complaints against MSCI, FTSE Russell, and S&P Dow Jones Indices for violating OECD Guidelines for Multinational Enterprises on Responsible Business Conduct. As the complaints explain, the firms did so by promoting ESG-labeled investment in companies linked to Myanmar’s military, despite its history of abuses, including the Rohingya genocide and ongoing violent crackdown on pro-democracy activists. The complaints, filed jointly with our partners ALTSEAN-Burma and Blood Money Campaign of Myanmar, were submitted to the U.S., U.K., and Dutch National Contact Points for Responsible Business Conduct (NCPs), which are government offices tasked with handling complaints alleging noncompliance with the OECD Guidelines for Multinational Enterprises.

Read the complaints here.

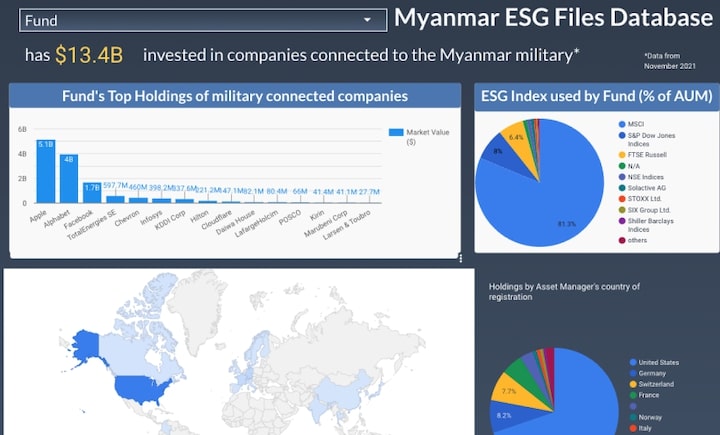

The complaints are based on extensive research revealing that MSCI, FTSE Russell, and S&P Dow Jones Indices had collectively put 23 military-linked companies on their ESG indexes, greenlighting them for inclusion in ESG-labeled funds, including funds managed by BlackRock, Deutsche Bank, Northern Trust, State Street and Vanguard. In total, we found that ESG indexes managed by MSCI, FTSE Russell and S&P Dow Jones Indices had directed $13.7 billion in equity investments to the 23 companies doing business with the military. Companies benefiting from this so-called “responsible investment” include weapons dealers arming the regime, tech firms serving the military-controlled national police force, and others that direct profits and resources to the military, allowing it to violently crush dissent and maintain its grip on power.

The complaints outline how each of the three firms has failed to uphold its human rights due diligence responsibilities and failed to use the considerable leverage it has over companies listed on its ESG indexes to address serious human rights risks and impacts stemming from those companies’ ties to the Myanmar military.

Inclusive Development International began engaging with MSCI, FTSE Russell and S&P Dow Jones Indices about their role directing ESG-labeled investment to Myanmar military-linked companies years before filing complaints against them. When we first published research, as part of our Myanmar ESG Files report, showing that they were including problematic companies in their indexes, we reached out to all three index providers to share our findings and discuss the steps they could take to fulfill their responsibilities under the UN Guiding Principles on Human Rights and the OECD Guidelines. Unfortunately, none of the three firms has given any indication since then that it is taking steps to fulfill those responsibilities.

Inclusive Development International first published research on ESG-labeled investment going to companies linked to human rights abuses in 2022. The Myanmar ESG Files database provided detailed information on hundreds of ESG-labeled funds we had found were invested in companies with ties to Myanmar’s military—including the specific companies they were invested in, those companies’ links to the military, the total value of each fund’s holdings in those companies, the asset managers overseeing the funds and the ESG index providers and rating and research firms those asset managers relied on. The accompanying Myanmar ESG Files report exposed the systemic issues within the ESG investing industry that allowed this to happen. The report included a specific focus on the role of ESG index creators and called on them to exclude any company from their ESG indexes if it refused to stop facilitating human rights abuses in Myanmar.